Lo sa bene l’ex PdC: internet, i microchip, l’IoT e, forse, l’AI. Il Vecchio Continente ha perso già troppe sfide. Una delle poche, pochissime, rimaste è quella dello spazio, la grande opportunità per la potenza di un tempo. Scrive nel rapporto (che potete scaricare qui):

The value of the space economy is substantial, and is set to grow significantly with the adoption and implementation of space solutions across more and more sectors in the broader economy. The value of the global space economy in 2023 stood at USD 630 billion and estimates for the future indicate that it could reach USD 1.8 trillion by 2035, growing at an average of 9% per year. […] In terms of creating new markets and generating value-added – the estimated value of the sector already stands at over USD 3 trillion.

1800 miliardi. Una piccola fetta basterebbe per saziare i bisogni di un qualsiasi stato, ma Super Mario ha altri piani: l’Europa, per quello che è il suo capitale umano deve essere nelle condizioni di giocare a testa alta con gli altri grandi player, USA e Cina in primis.

Per Draghi è essenziale la novità di questi anni dove “Il New Space sta trasformando radicalmente l’industria spaziale, che si sta orientando verso nuovi schemi di finanziamento (finanziamenti privati), l’apertura al rischio, la consegna rapida di prodotti e servizi e la riduzione dei costi”, “i grandi progetti spaziali non si baseranno solo su partenariati tra più Paesi, ma si prevede che saranno guidati anche da partenariati pubblico-privati, gruppi di Paesi più piccoli, domanda commerciale e soluzioni”. E tutto questo è pronto ad esplodere in vista del pensionamento della ISS, concordato per il 2031.

Per Draghi l’Europa può farcela:

The EU has developed world-class strategic space assets and capabilities, with technical competences on par with other space powers in most areas. The EU is a space power with significant industrial capabilities and know-how, particularly regarding the assembly and integration of systems. […] More than 250,000 highly skilled jobs are directly supported by the EU Space Programme with estimated value-added between EUR 46 and 54 billion. […] European companies are leaders in satellite manufacturing.

e ancora

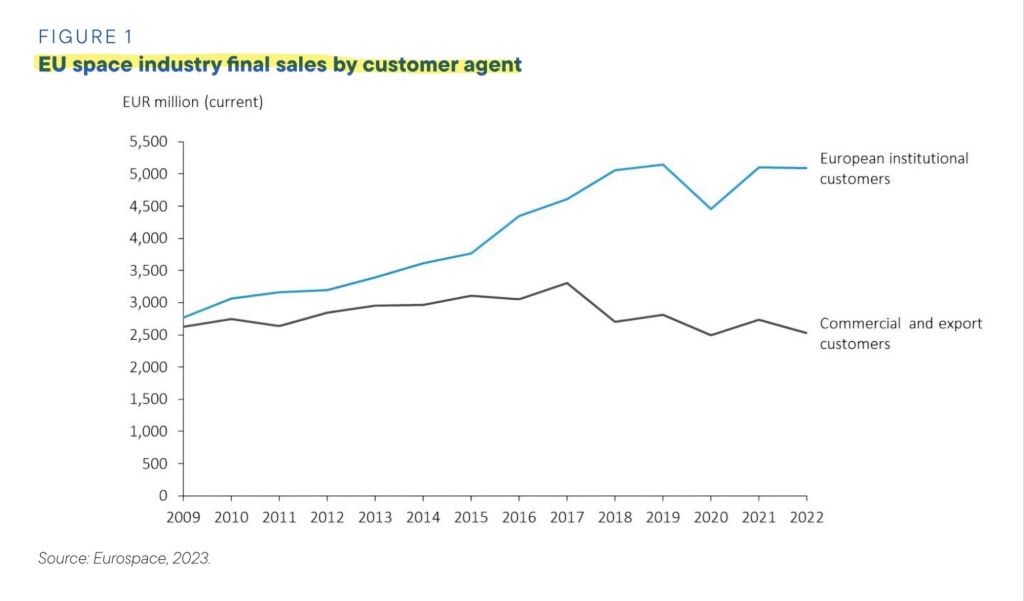

Overall, the European space industry has remained competitive during the past decades. This is noteworthy especially considering that the share of public funding has been considerably lower compared to that of its main competitors. […] The New Space ecosystem is also booming in the EU, with more than 800 space companies created in the last decade, some of which are the most innovative worldwide.

“Tuttavia, l’UE ha probabilmente perso terreno nelle attività spaziali e un ulteriore ritardo potrebbe tradursi rapidamente in una maggiore dipendenza strategica” che già si è verificata a causa di problemi e ritardi con i lanciatori europei Ariane 6 (che sostituisce Ariane 5, debuttato nel ’96)e Vega C (che sostituisce Vega, debuttato nel 2012).

Per approfondire la crisi dei lanciatori europei potete consultare il Box 1 alle pagine 175-176 del rapporto.

E ovviamente tutto questo a causa dei pochi investimenti:

The EU’s industrial base suffers from forty years of investment, which on average ranged between 15% and 20% of that in the US. […] In 2023, public expenditure on space in the EU and its Member States accounted for about USD 13 billion, compared to the US’ USD 73 billion, i.e. more than five times larger. Budgetary projections indicate that the US government’s space expenditure is expected to continue increasing, while European funding will stagnate. China is expected to overtake Europe in the next few years, reaching an expenditure of USD 20 billion by 2030.

Quindi l’ex banchiere propone un fondo che permetterebbe alla commissione europea di agire dacliejte di ancoraggio per acquistare servizi e prodotti sul mercato UE. Il fondo ha anche gli obbiettivi di finanziare progetti di collaborazione multinazionali, attrarre finanziamenti privati (che aumentano quando lo stato investe in un settore, agendo da fattore di sicurezza e stabilità) e “acquisire aziende strategiche e critiche sul mercato europeo che rischiano di essere acquisite da entità extra-UE, per garantire la sicurezza economica e l’autonomia strategica dell’UE nelle tecnologie spaziali chiave”. E questo ultimo punto è affrontato in un passaggio fondamentale da Draghi:

The space sector is high-tech and capital intensive with long investment cycles and, therefore, high risk. European companies are not able to scale up mainly due to limited access to finance. They are as a result forced to turn to non-EU markets for growth financing, often losing their EU ownership. They are also being bought by large non-EU companies, which acquire technology and know-howinitially developed in the EU.

L’accesso limitato ai finanziamenti è dovuto all’ “avversione al rischio dei player istituzionali chiave come la Banca Europea per gli Investimenti (BEI)”. Infatti:

US private investments in space totalled approximately EUR 4 billion, compared to EUR 1 billion in Europe. The private investment gap in Europe is estimated at EUR 10 billion during the next five years. Compared to previous years, as of 2023, private investment in the space economy have started to be more selective and targeted, decreasing access to finance for many emerging players.

Super Mario sa bene però che è inutile immettere fiumi di denari in un settore, servono riforme strutturali, i soldi sono solo l’olio che non fa cigolare la porta.

Is fair to say that NASA and the Space Force are the main two arms of the US government for space matters. They manage most of the approximately USD 50 billion a year spent on space, with the US Vice-President in charge of relevant policy […]. The institutional set-up for space policy in Europe is more complex and fragmented compared to the US.

In Europa infatti le competenze sono frammentate in modo importante per la presenza degli stati autonomi e a livello europeo sono frammentate tre Commissione, l’ESA e l’Agenzia UE per il Programma spaziale (EUSPA)

L’ex banchiere parla anche di “introdurre norme mirate sulle preferenze europee per il settore spaziale a sostegno delespansione delle imprese europee” e “eliminare il principio del ritorno geografico dell’Agenzia spaziale europea per ridurre la frammentazione della base industriale dell’UE e modernizzare le norme UE sugli appalti”. Su quest’ultimo punto il rapporto spiega che:

During the past decades, the principle of geographical return has enabled the commitment of significant national budgets to common space programmes. It has also allowed the increase of the capabilities of member countries in developing space tech nologies and enabled their industry to engage in different space technology fields and value chains. However, this policy is increasingly outdated.

Il meccanismo di ritorno geografico degli investimenti, che dà agli stati la sicurezza che ogni euro investito tramite la piattaforma europea vada a creare posti di lavoro nel proprio territorio, non funziona più. Questo per diversi motivi, ne ho selezionati due:

- Uno squilibrio tra gli attori industriali più competitivi e l’effettiva allocazione delle risorse

- Vincoli sulla scelta dei fornitori e sull’impossibilità di cambiare fornitore in caso di prestazioni insufficienti, con un impatto sulle tempistiche e sui costi del progetto

Il rapporto sottolinea anche come gli “attori privati globali nel settore spaziale, non seguono alcuna logica geografica non commerciale all’interno di un mercato unico”.

La sfida è ardua, ma l’Unione può farcela. L’impegno però è necessario, imminente. Ora. Ora. Ora o mai più.

Europe is home to world-leading research institutions and universities, with a high impact on research and scientific progress in space. Altogether, investment in Europe by the EU, the ESA and major European countries in the field of space (Germany, Spain, France, Italy, and the UK) amounted on average to EUR 2.8 billion per year between 2020 and 2023. At the same time, investment in the US and China totalled EUR 7.3 billion and EUR 2.3 billion respectively. There is a pressing need to increase public investment supporting R&l in the field of space. Increased investment would not only enhance the competitiveness of the EU’s space sector at large, but also foster the development of future stra tegic capacities, such as in-space operations and services (e.g. spacecraft servicing, assembly, manufacturing and transport in space) and quantum technologies.

Lascia un commento